“Tariff is a word most of us first heard in high school history class. We remember something about the Smoot-Hawley Tariff Act of 1930, the Great Depression and the dark side of protectionist trade policy,” according to Capital Group economist Robert Lind. “Fast forward to today and tariffs are once again taking center stage, serving as the linchpin of President Trump’s trade policy – and as a cause of sharply rising market volatility. A fierce debate has emerged over the impact they could have on the global economy. Critics argue these tariffs mark the start of a new trade war that will hurt all countries in the end. Supporters say it’s an attempt by the U.S. to reduce long-term trade deficits and compel other countries to lower their own protectionist measures. In either case, the rewiring of global trade reflects a larger shift in the geopolitical world order.”

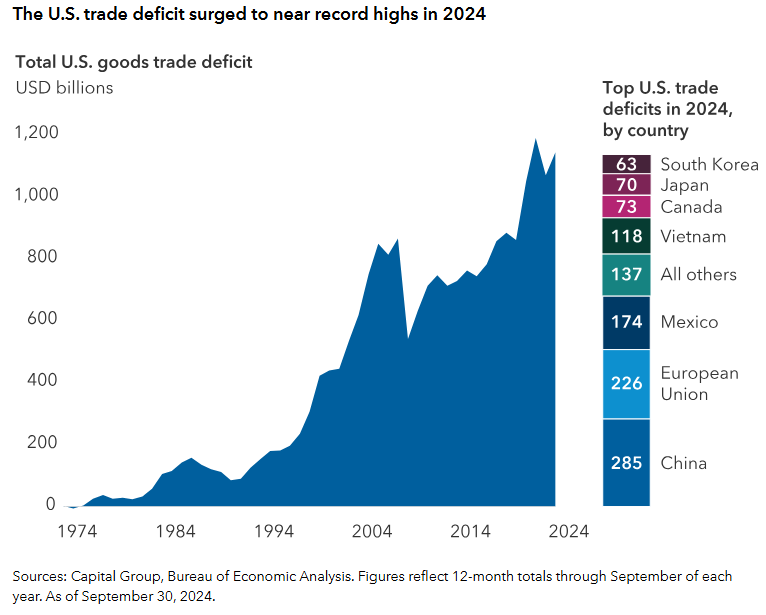

Tariffs have dominated the headlines and caused markets to significantly drop this week. But hasn’t the Administration discussed and campaigned on these for months? Why are markets reacting so negatively? Well, the Administration elected to go big and incredibly bold on the tariffs. A baseline 10% tariff will go into effect tomorrow for all imported goods. Reciprocal tariffs will also be added to specific countries. Rather than using the typical quoted tariff rate to determine the reciprocal rate, they elected an unorthodox calculation which included the trade deficits in the chart below. These are much higher than markets originally anticipated which contributed to the spike in volatility. This creates significant uncertainty in relation to global growth, inflation, company earnings and increases the chance of a recession.

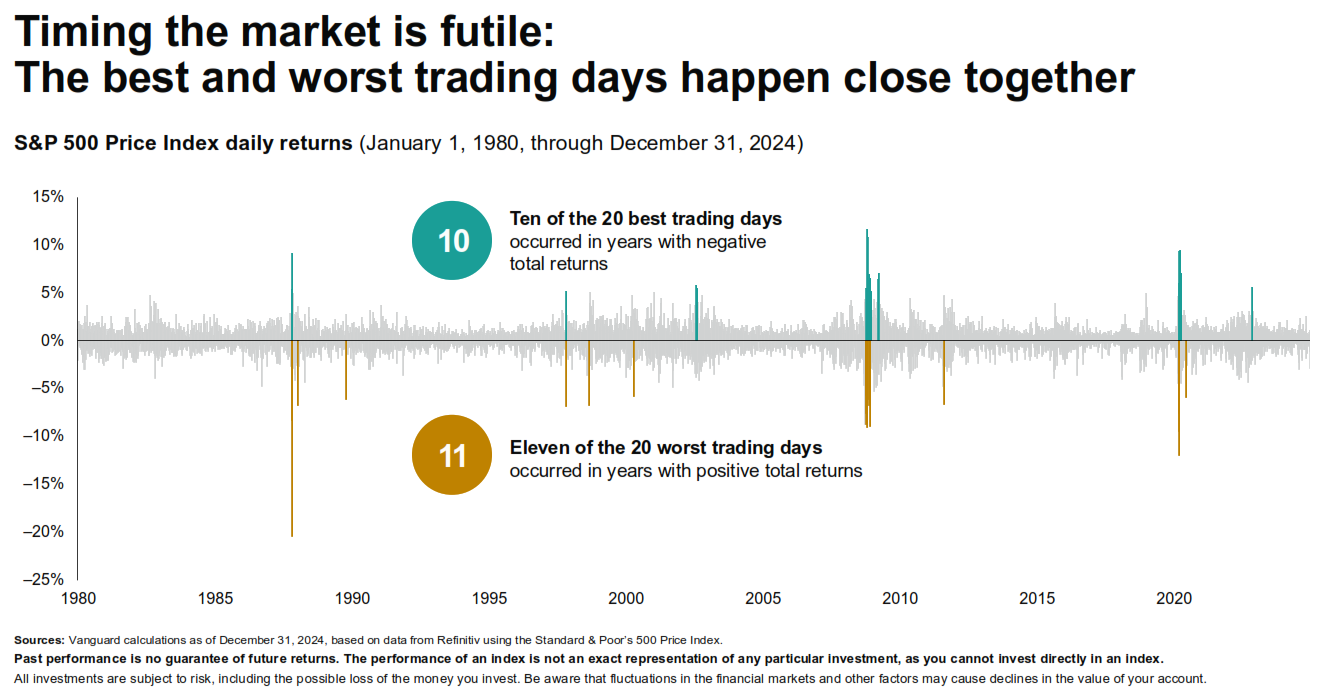

Yesterday was the worst day for domestic stocks since COVID and today looks like it could be the same. Many investors might wonder if it’s prudent to exit stocks and sit on the sidelines until this turmoil subsides. However, it’s very difficult to successfully time this. For example, the Vanguard chart below shows how the worst days in the market tend to cluster around the best days. It’s next to impossible to avoid these poor days and still get the best ones.

We remind clients to look at the bigger picture through the lens of their financial plan. Yes, markets are down, but the S&P 500 was still up 6% over the past year and the 3-year annualized return is still over 7% as of this morning. International stocks have been a bright spot with 4-8% YTD bounces. Lastly, bonds have served as a ballast to portfolios and delivered 1-4% YTD growth.

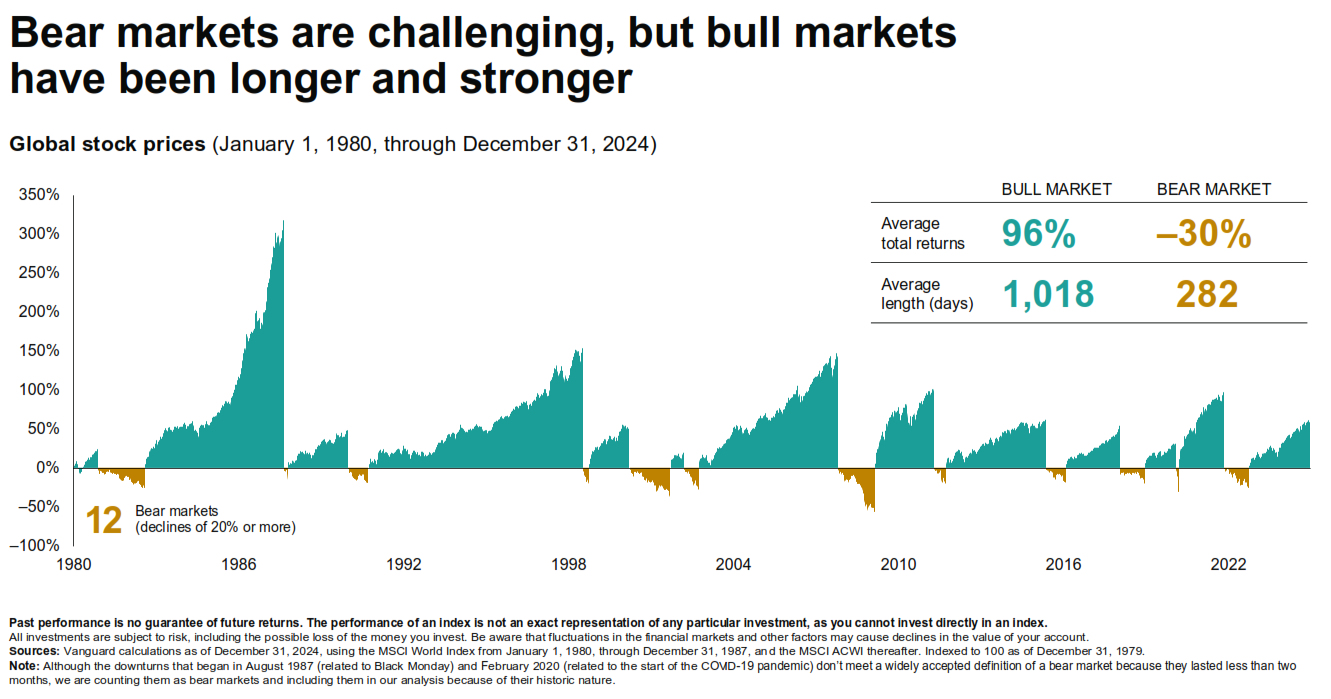

We will likely continue to see very choppy markets dominate the headlines as they grapple with the true impact of these tariffs. The lesson may be that in times like these, it’s important to be clear about what we do and don’t know — recognizing that tariffs are just one part of the equation. Ultimately, the U.S. stock market has proven to be remarkably resilient over time as shown in the Vanguard chart below. Focusing on investment principles such as diversification and staying invested in the face of market volatility become more essential to achieving long-term investment goals.

In closing, is what we are facing today as perilous as World War II, the Korean or Vietnam Wars, the Great Recession, or more recently COVID-19? We don’t think so and the market has survived, and subsequently thrived when viewed through a long-term lens. It is true our worst fears lie in anticipation. We would encourage maintaining the long view but know we are here to address your questions and concerns.

IMPORTANT DISCLOSURE INFORMATION: Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by PDS Planning, Inc. [“PDS”]), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from PDS. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. PDS is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice. A copy of the PDS’ current written disclosure Brochure discussing our advisory services and fees is available for review upon request or at www.pdsplanning.com. Please Note: PDS does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to PDS’ web site or blog or incorporated herein, and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly. Please Remember: If you are a PDS client, please contact PDS, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian.